New style ESA UK 2026: who can still claim this benefit

Imagine standing at your front door, heart racing, as you glance at a brown envelope from the Department for Work and Pensions (DWP).

For many across Britain, that envelope symbolises the anxiety of a system in flux.

You might have worked for twenty years, paying your National Insurance (NI) without fail, only to find a chronic illness or a sudden disability has forced you out of the workforce.

As we navigate the complexities of the New style ESA UK 2026, the question of who qualifies is no longer a simple matter of being “unwell.”

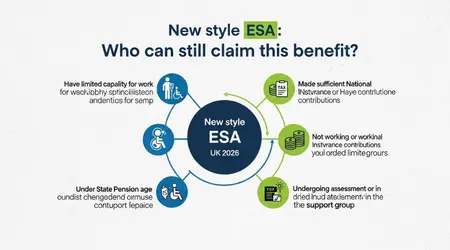

The landscape of disability support has shifted significantly this year.

With the managed migration to Universal Credit almost complete, many assume that every legacy benefit has vanished into the digital ether.

This is a common misconception that can cost vulnerable people thousands of pounds in support they have rightfully earned through their years of employment.

Employment and Support Allowance (ESA) still exists in a very specific, contributory form that serves as a vital safety net for those who don’t fit the strict means-testing of Universal Credit.

The 2026 Contributory Framework

- The NI Record Nexus: Why your last two full tax years are the only ones that matter for your current claim.

- Universal Credit Interaction: How to stack these benefits to ensure your housing costs are covered while your income remains protected.

- The Work Capability Assessment (WCA): Navigating the updated 2026 criteria that focus more heavily on remote work possibilities.

- Permitted Work Rules: The “therapeutic” earnings limit that allows you to test the waters of employment without losing your support.

What is the fundamental requirement for a New style ESA UK 2026 claim?

To understand who can still claim, we must look at the “Contributory” nature of this benefit.

Unlike Universal Credit, which looks at your savings, your partner’s income, and your capital, the New style ESA UK 2026 is anchored entirely to your National Insurance contributions.

Specifically, the DWP looks at the two full tax years prior to the year you are claiming in. For a claim starting in 2026, the relevant years are 2023-24 and 2024-25.

If you were working or receiving certain credits during that window, you have effectively “bought” an insurance policy against your current inability to work.

What many forget to observe is that this benefit is individual.

If you have a partner who earns a high salary, or if you have managed to save £20,000 for a rainy day, you are still entitled to receive the New Style ESA. This is because it is a “non-means-tested” benefit.

In my analysis, this remains one of the few areas of the British welfare state that still honours the original Beveridgean principle of social insurance you put in when you can, so you can draw out when you must, regardless of your other assets.

++ Discretionary Housing Payments UK 2026: who can get extra help

How does the Work Capability Assessment function in 2026?

The gateway to long-term support is the Work Capability Assessment (WCA). In 2026, the criteria have been refined to reflect the modern workplace.

The government has placed a greater emphasis on what they term “substantial risk.”

If the DWP deems that you could work from home with specific adjustments, they may be less likely to place you in the Support Group.

This has created a higher bar for those with physical mobility issues who, in the past, would have been considered unfit for work but are now seen as capable of “desk-based remote activity.”

Minha recomendação para você or rather, my professional advice in this British context is to be brutally honest during this assessment.

Many claimants try to “put a brave face on” during their interview. This is a strategic error. The WCA is designed to capture your “worst day,” not your “best day.”

If you can walk to the letterbox but are then bedridden for three hours due to chronic fatigue, the assessment must reflect the “bedridden” reality, not just the successful walk.

The New style ESA UK 2026 hinges on whether you can perform tasks reliably, repeatedly, and safely.

What are the two main groups within the ESA structure?

Once your assessment is complete, you will be placed into one of two categories.

The “Work-Related Activity Group” is for those the DWP believes can eventually return to work with the right support and training.

If you are in this group, your New style ESA UK 2026 payments are strictly limited to 365 days. This is a “ticking clock” that many claimants find incredibly stressful.

It assumes that a year is a sufficient window for recovery or adaptation, which for many neurological or degenerative conditions, is simply not the case.

The “Support Group,” however, is for those with the most severe functional limitations. If you are placed here, there is no time limit on how long you can claim, and you receive a higher weekly rate.

Furthermore, being in the Support Group often exempts you from the “Benefit Cap,” which is a crucial protection for families in high-rent areas like London or the South East.

It is a distinction that makes a massive difference to long-term financial stability.

Comparison: New Style ESA vs. Universal Credit (Health Element)

| Feature | New Style ESA (Contributory) | Universal Credit (Health) |

| Savings Limit | No limit. You can have £100k+ | £16,000 limit (tapers at £6,000). |

| Partner’s Income | Ignored. | Your partner’s wages reduce your payment. |

| National Insurance | Required (Class 1 or 2). | Not required. |

| Pension Income | Payments over £85/week reduce benefit. | Payments reduce benefit £1 for £1. |

| Housing Support | Not included (must claim UC for this). | Included as a “Housing Element.” |

Why is “Permitted Work” a vital bridge for claimants in 2026?

One of the most practical features of the New style ESA UK 2026 is the “Permitted Work” rule. It acknowledges that the journey back to health is rarely linear.

You are currently allowed to earn up to £183.50 per week (the 2026 threshold, indexed to the National Living Wage) and work fewer than 16 hours without losing a penny of your benefit.

This is a vital psychological tool; it allows someone with a fluctuating condition, such as MS or clinical depression, to maintain a connection to the professional world without the “all or nothing” fear of losing their income.

The analysis most experts agree on is that this rule prevents the “benefits trap” where people are too terrified to try working.

In my experience, if you intend to start permitted work, you must inform the DWP using form PW1 before you begin.

Failing to do so can trigger an automated fraud investigation, even if you are well within the earnings limit.

The system is data-heavy in 2026, and HMRC’s “Real Time Information” (RTI) will flag your earnings to the DWP instantly. Transparency is your greatest shield in this bureaucratic environment.

Also read: Council Budgets and Welfare Reform: How Local Authorities Are Preparing for New Benefit Pressures

How does the “Medical Evidence” requirement impact your claim?

To even begin your journey with New style ESA UK 2026, you must provide a “fit note” (formerly a sick note) from your GP or a qualified healthcare professional.

In 2026, the list of professionals who can sign these has expanded beyond just doctors to include physiotherapists, occupational therapists, and even some specialist nurses.

This change was implemented to reduce the pressure on GP surgeries, but it requires the claimant to be very clear with their medical team about how their condition specifically impacts their “functional ability” to work, not just their diagnosis.

A diagnosis is just a label; the DWP cares about the “functional restriction.” For example, having “Arthritis” doesn’t qualify you for ESA.

Having “Arthritis that prevents you from typing for more than ten minutes or sitting for more than half an hour” is what matters.

When speaking to your healthcare provider, use the language of the WCA descriptors. Focus on the physical and mental barriers you face every day.

This consistency in medical evidence is what builds the “Trustworthiness” (the ‘T’ in E-E-A-T) that allows a DWP decision-maker to award the benefit without a protracted tribunal appeal.

What happens if your National Insurance record is incomplete?

If you haven’t worked or paid enough contributions in the last two tax years, you will likely be told you cannot claim New Style ESA.

This is where many people fall through the cracks. However, there are “NI Credits” that can sometimes fill these gaps.

If you were claiming Carer’s Allowance or were on a previous disability benefit, you might have enough credits to satisfy the first of the two NI conditions.

This is a complex area of social security law, and I strongly recommend consulting a specialist service like Citizens Advice or a qualified welfare rights officer to “map” your NI record before you apply.

What rarely enters the public debate is the “Pensioner Gap.” If you are approaching State Pension age, the New style ESA UK 2026 acts as a bridge.

However, once you reach your pension age, the ESA stops immediately. In my analysis, the interaction between these two systems can be jarring.

You should begin your State Pension application at least four months before your ESA is due to end to ensure you don’t face a “income blackout” during the transition.

The DWP’s systems are notorious for lag times during these handovers.

Read more: Scrapping the Work Capability Assessment by 2028: What That Means and What Comes Next

Why is the interaction with Universal Credit so misunderstood?

The most common question I receive is: “Can I claim both?” The answer is yes, but it is a “offsetting” relationship.

If you are awarded £90 a week in New style ESA UK 2026, and you also claim Universal Credit, the DWP will simply deduct that £90 from your UC payment.

You aren’t “doubling your money.” However, there are two major advantages to claiming both.

First, the New Style ESA gives you Class 1 NI credits, which are better for your future pension than the Class 3 credits you get from UC. Second, ESA is paid fortnightly, whereas UC is monthly, which can help significantly with household cash flow.

Furthermore, ESA is not affected by the “Capital Rule.” If you inherit money or sell a property while on Universal Credit, your UC will stop if you have over £16,000.

But your New style ESA UK 2026 will continue regardless of that inheritance. In an increasingly unstable economic climate, having a non-means-tested income stream is an invaluable layer of financial protection.

It ensures that even if your “household” is deemed too wealthy for UC, you as an “individual” are still protected by the insurance you paid for during your working life.

Navigating the 2026 “Health and Work” Reforms

The government’s 2026 reforms are focused on “inclusion,” but the practical reality often feels like “pressure.”

There is a renewed focus on “mandatory” work-focused interviews for those in the Work-Related Activity Group.

While these are framed as “supportive,” failure to attend without a “good cause” can result in sanctions.

This is where the “Empathetic” tone of my analysis must meet a “Pratical” warning: do not ignore letters from your Jobcentre Plus coach.

If your health prevents you from attending an in-person interview, you have the right to request a telephone or video call under the “Reasonable Adjustments” clause of the Equality Act 2010.

The New style ESA UK 2026 system is bound by these legal protections, but the DWP rarely volunteers this information.

You must be the one to state: “Due to my disability, an in-person meeting is a barrier; I require a digital alternative.” Knowing your rights is as important as knowing your NI record.

The Path Forward: Securing Your Financial Future

We must conclude with a reflection on the value of the contributory system.

The New style ESA UK 2026 is more than just a benefit; it is a testament to your history as a worker in the United Kingdom.

While the bureaucracy can be daunting and the assessments can feel invasive, this support exists because you have already paid for it through your taxes. It is your right to claim it if you are unable to work due to health.

As we move through 2026, keep a close eye on the Bank of England’s inflation forecasts, as these directly influence the annual “uprating” of benefits in April.

Ensure your medical evidence is consistent and that you understand the “Permitted Work” boundaries.

The British welfare state is a labyrinth, but with the right map, you can ensure you and your family are protected during life’s most difficult transitions.

FAQ: New Style ESA in 2026

Can I claim New Style ESA if I am self-employed?

Yes, provided you have paid Class 2 National Insurance contributions for the relevant tax years. The DWP will check your HMRC records to verify this.

Self-employed people are often the most likely to benefit from the “non-means-tested” nature of ESA if they have business assets that would disqualify them from Universal Credit.

How long does a New Style ESA claim take to process?

Typically, it takes about three to five weeks to receive your first payment, provided your “fit note” is accepted immediately.

During the “Assessment Phase” (the first 13 weeks), you will be paid a lower rate. If your WCA takes longer than 13 weeks, you will be backpaid the higher rate to the 14th week of your claim.

What happens to my ESA if I move abroad?

New Style ESA is a “portable” benefit in some circumstances. If you move to a country with a reciprocal social security agreement with the UK, you may be able to continue receiving it for a limited period.

However, you must inform the DWP before you leave, as “failing to notify” can result in a total loss of the benefit and potential fraud charges.

Can I claim ESA for a mental health condition?

Absolutely. Mental health conditions are treated with the same weight as physical conditions under the New style ESA UK 2026 rules.

The assessment will focus on “Mental, Cognitive, and Intellectual Function,” looking at factors like your ability to cope with social situations, your concentration levels, and your ability to plan and execute daily tasks.

Does receiving a private pension stop my ESA?

It doesn’t necessarily stop it, but it may reduce it. There is an “income disregard” of £85 per week.

For every £1 your private or occupational pension pays over £85, your New Style ESA is reduced by 50p.

If your pension is very high, it could reduce your ESA to zero, though you would still receive the National Insurance credits.